Oh, how the tides have turned.

For the last decade, investors would have preferred to have their eyeballs gnawed out by an angry beaver while riding a seatless unicycle rather than buying international companies. In other words, investors avoided international investment at all costs.

Oh, how the tides have turned in 2025:

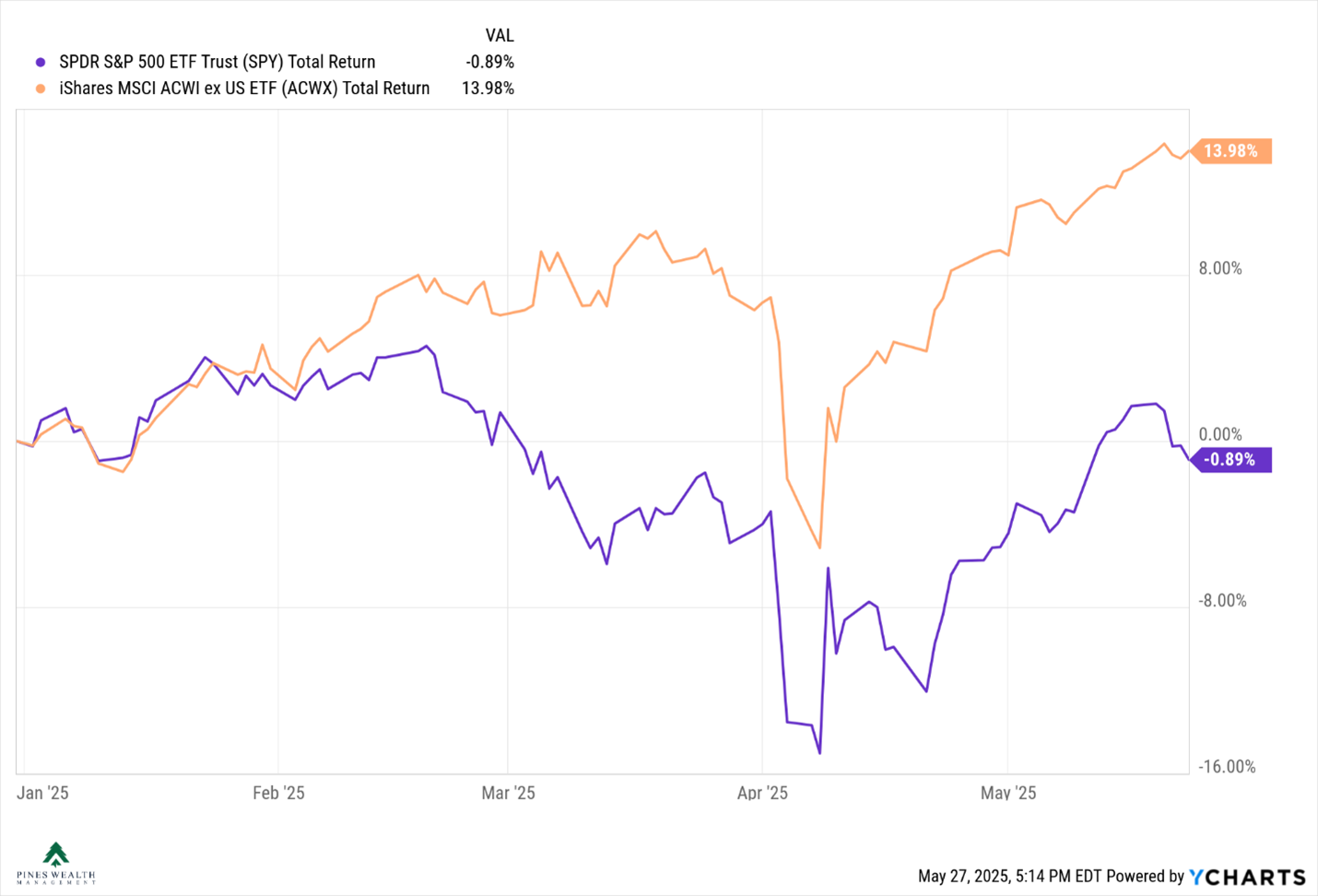

So far in 2025, the performance gap between these two asset classes is one of the most notable on record.

Investors find themselves looking around asking – what in the hell is happening with US companies compared to their international counterparts?

What’s the main driver of this gross outperformance?

As usual, there is not one clear answer.

There are several data points that may help to explain what is happening with international this year, so let’s get into the weeds:

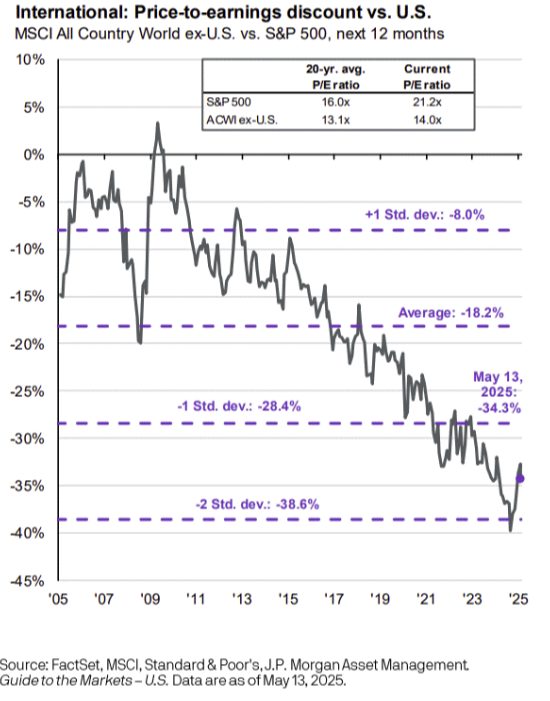

International Companies are selling for cheaper valuations than their US counterparts –

After a decade or more of international being the red-headed stepchild of investing, investors are looking for value.

It's not surprising, given the tech sector has dominated portfolio returns for the better part of a decade. Investors came into the year wondering if AI companies could keep up their torrid pace of earnings growth,

Meanwhile, international companies are selling for a 30% discount to their US brethren:

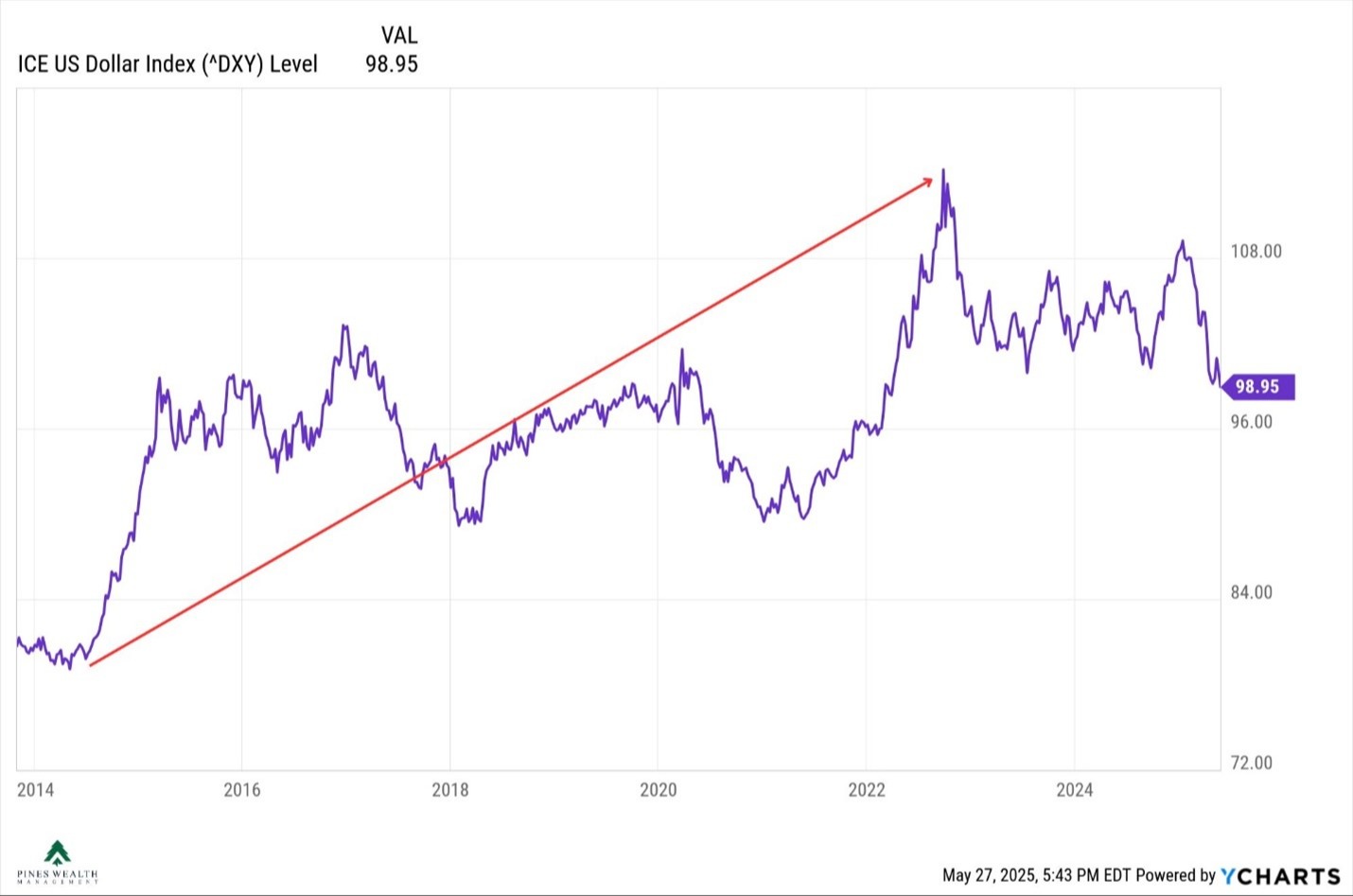

The dollar is weakening –

The dollar index (DXY) strengthened over the last decade, attracting foreign investors to US companies. However, since 2022, the dollar has struggled.

Periods of a falling US dollar have historically coincided with periods of international equity outperformance.

While I’m not even remotely ready, and neither are investors to shovel dirt on the dollar as the world’s reserve currency, it’s notable that the dollar is stuck in a narrow range and is certainly off its 2022 highs—something to keep an eye on.

The performance of international companies so far this year doesn't appear to be a one-off –

If this were a hiccup for US companies, we wouldn’t be seeing structural catalysts deep within the European countries and their Japanese counterparts.

Both Europe and Japan are getting serious with reforms to their corporate governance.

They are significantly increasing their defense spending, and they are finally getting serious about developing new energy infrastructure. Both areas have become top priorities and have the potential to become long-term tailwinds for international companies.

While I am by no means encouraging investors to chuck their asset allocation plan within their financial plan and to invest the motherload in international companies, it might be an opportunity to increase your weighting in international (if you haven’t already).

It's clear that YTD international has thumped its US counterparts, but the magnitude is small in the context of confirming a longer-term trend.

Stay the course, my friends.